| Exam Name: | WGU Accounting for Decision Makers C213 VAC2 | ||

| Exam Code: | Accounting-for-Decision-Makers Dumps | ||

| Vendor: | WGU | Certification: | Courses and Certificates |

| Questions: | 69 Q&A's | Shared By: | katherine |

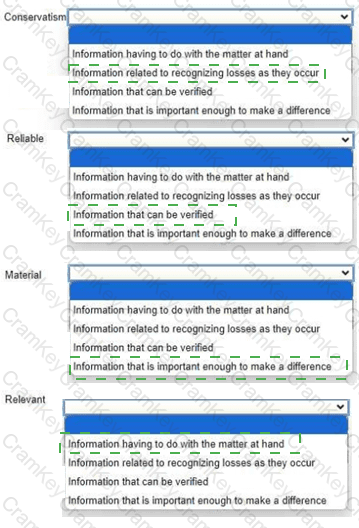

Match each accounting term with its definition.

Answer options may be used more than once or not at all.

Select your answer from the pull-down list.

Which internal control is intended to ensure that a company does not mistakenly pay a supplier for an invoice that includes more items than were actually received?

Which action should a managerial accountant consider taking if confronted by an ethical conflict?

Which events represent financial information recorded in the accounting system of a business?

TESTED 27 Jul 2026